Investing in IPO’s and SPAC’s on Day 1 and Beyond

Investing in IPO’s and SPAC’s on Day 1 and Beyond

SPAC's are growing in popularity, but are they worth they hype?

About a year ago, I wrote an article about how the IPO market was broken. Since that article, we continue to see a trend of mispriced IPO’s including Airbnb, DoorDash, and Snowflake that were severely undervalued. This resulted in founders of companies leaving a lot of money on the table.

“I don’t want to say that the market is broken, but the process of how we’re doing these deals is definitely broken,” Cramer said.

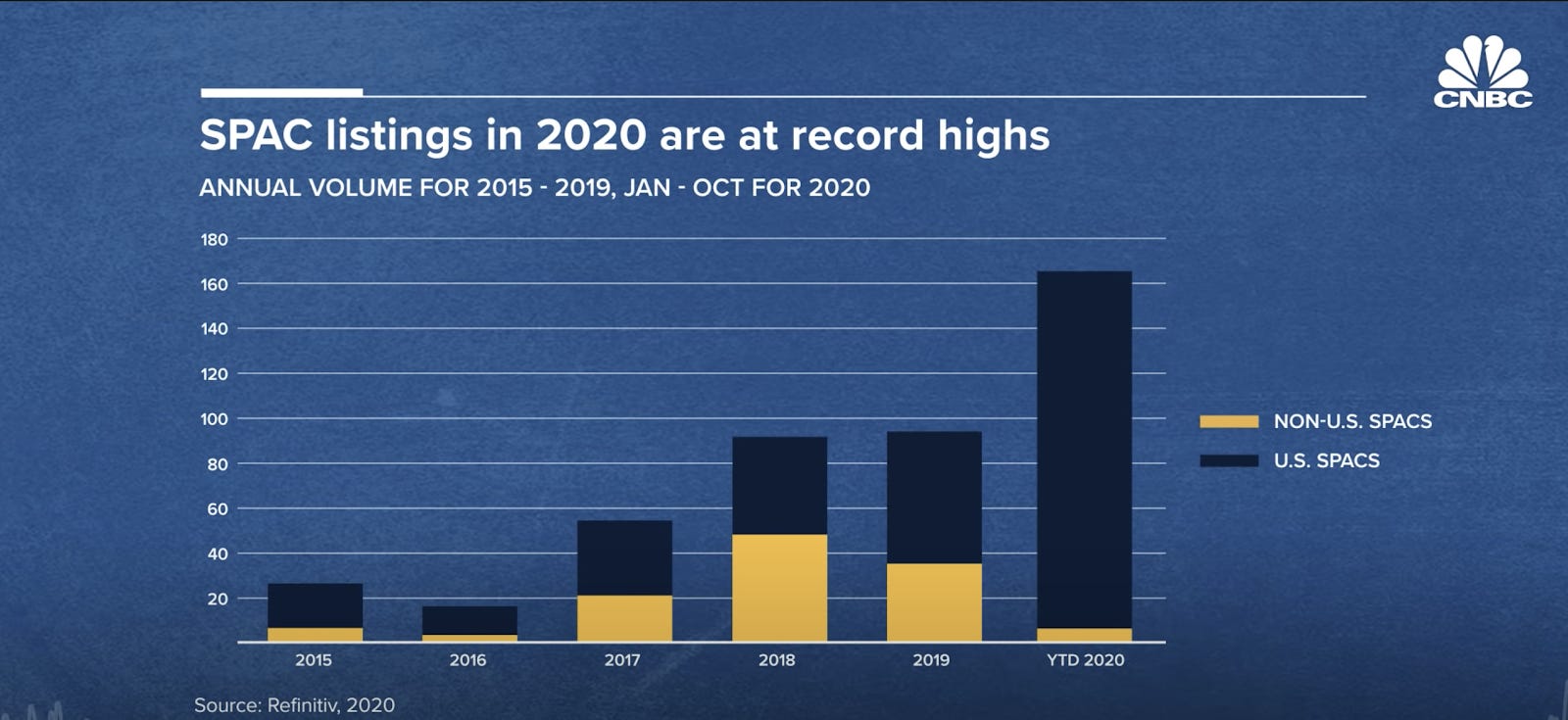

This is also a big reason why many companies are going the SPAC route.

A SPAC, often called a reverse IPO or a blank check company, is almost the exact opposite of an IPO. With a SPAC, the investors raise money first and go public at a defined price, usually $10, and then they find an acquisition target.

Many companies on the path to IPO prefer a SPAC because it’s quicker, cheaper, cleaner (documentation-wise), no IPO window, and there is no threshold when a company can be SPAC’d vs an IPO.

So, instead of companies going through an extravagant and complex IPO roadshow, they get a cleaner approach to the market. SPACs can get done in 6 months when IPOs typically take about 18.

While Direct Listings also grew in popularity with Spotify, Asana, and Palantir all going through the Direct Listing route, the SPAC route is growing in popularity, especially in the last 6 months.

Here is a good summary of the fees between a traditional IPO, Direct Listing, and a SPAC.

So, the question is, is the SPAC worth it for all stakeholders involved?

Overall, SPAC Performance Is Neither Positive nor Negative.

If we take a look at the post-merger SPAC target performance by Bloomberg Law, you’ll notice that the performance is really a mixed bag.

What’s also interesting about SPAC’s is that even if they go public, it doesn’t mean there will always be an acquisition or sometimes called “de-SPAC’d”

Of all 117 SPAC merger deals—with an aggregate value of $99.3 billion—that were announced between Jan. 1, 2019 and Feb. 10, 2021, and for which definitive agreements have been entered into, 39 deals—with an aggregate value of $47.9 billion—have reached completion so far. [source]

14 out of 24 reported a depreciation in value as of one month following the completion of the merger. It’s true that, as of Feb. 10, the same group of companies has shown some improvement, with one-third reporting a year-to-date depreciation in value. But this doesn’t mean all have shown improvement.

So, SPAC’s aren’t showing any performance characteristics that would make a SPAC a slam dunk approach. SPAC’s are still no different than a traditional IPO in the sense that the market still determines the price in the end. It’s all about the road traveled to get there.

So, let’s talk a little bit about the road traveled IPO vs SPAC.

IS A SPAC WORTH IT FOR EVERYONE INVOLVED?

I ran some data from 2020 where I compared all companies that went public, whether through an IPO or a SPAC. For the sake of simplicity, I grouped traditional IPO’s and Direct listings as just IPO.

We would of course expect a SPAC to have very low volatility on IPO day because at that point it's an empty shell with a $10 price. If I buy a SPAC on IPO day, it’s a little like buying an option or a lottery ticket.

Here is what I uncovered.

Based on this analysis of opening day IPO’s, here are some of my thoughts.

IPO’s are still underpriced significantly.

When the closing price on the first day is 10% higher than the offering price, then that usually means the IPO was underpriced.

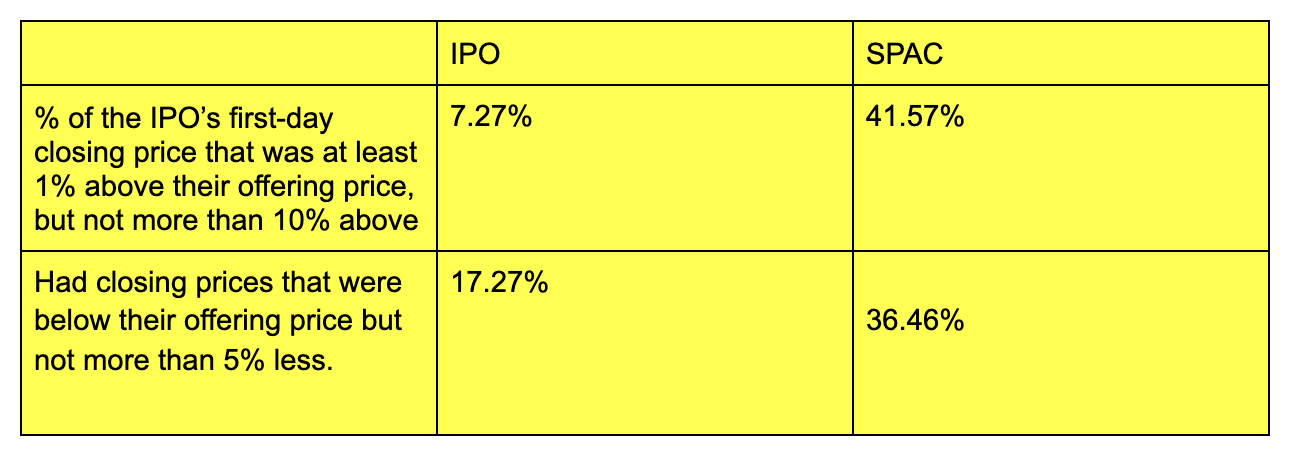

When I compared first-day closing price at IPO vs a SPAC, I found that 60% of IPO’s during my timeframe had a closing price higher than 10% of the offering price. SPAC’s had a 5.56% difference. That’s a big difference.

IPO’s being underpriced can cost the VC companies and founders significantly more than they bargained for, to the tune of hundreds of millions or billions of dollars.

Result: Many IPO’s are undervalued, with founders leaving money on the table. This is good for IPO investors and maybe retail investors if they can get in before the pop, but not necessarily good for the founders. SPAC’s openings usually stay in line with the opening price.

SPAC’s don’t have a wild % change on IPO day.

Based on this data, SPAC’s opening day closes are almost never above 10% gain, or more than a 5% loss. Again, none of this is really surprising since this is all pre-merger.

41.57% of the IPO’s first-day closing price was at least 1% above their offering price, but not more than 10% above. 36.46% had closing prices that were below their offering price but not more than 5% less.

That means that if you’re investing in a SPAC on day 1, don’t expect a wild swing either way.

If you’re investing in a traditional IPO, there is a 7.27% chance that the IPO will be between at least 1% above, but not more than 10% above. Additionally, there is a 17% chance that the closing price will be a loser, but not more than 5% on day 1 closing.

WHAT HAPPENS AFTER DAY 1 CLOSING? SHORT-SELLERS. THAT’S WHAT HAPPENS.

Because of the nature of SPAC’s, more early-stage, riskier companies can be traded publicly without going through the due diligence of a traditional IPO price. So, while the initial SPAC price stays fairly consistent based on day 1 opening close data, this is all prior to an actual company being acquired.

And when there’s risk involved, you can bet that short-sellers will be there betting that the price goes down.

However, based on the data from JP Morgan, SPAC investors are doing well, but when compared against the S&P 500 during the same time period they were down 7%.

The typical buy-and-hold SPAC investor earned a 45% gross return between Jan. 1, 2019, and Jan. 22, 2021, Michael Cembalest wrote in a recent JPMorgan analyst note. (The analysis measures returns for the median investor.)

However, investors would have earned a higher return in the S&P 500 stock index, which yielded 52% over the same time period.

So, in the end, the investor returns are still not wildly different. As more “risky” companies go through a SPAC, it will be interesting to see how the returns change.

Who benefits from a SPAC?

The reality is both routes have their pros and cons. If you’re a company going through an IPO, you have to pay the fees to the banks. If you’re going to the SPAC route, you give up equity to the SPAC sponsor, but your pre-IPO life becomes a lot easier.

In all cases, it’s possible to be a win-win for the companies, VC’s and retail investors. Regardless of the chosen method, most stakeholders are making out OK in this very frothy market.

One theoretical value afforded to retail investors from a SPAC is the opportunity to acquire equity in a company at an earlier stage of its lifecycle. As the time between a company’s formation and its public trading debut increases, the financial returns created by the early rapid growth go to the VC and PE investors.

If SPAC sponsors can continue to find early-stage companies looking to go public, their retail investors can experience a little of the largesse typically afforded those Walls Street types who are spoken of so fondly on the Subreddits.

I suspect we will continue to see tech companies, especially crypto companies, go the SPAC route, just to avoid the traditional banking system that seems to be motivated to underprice stocks and add a lot of paperwork upfront.

It will definitely be an interesting 2021.